How To Deal with Aggressive Debt Collectors: Your Rights and Action Plan

Dealing with debt is hard enough, but aggressive debt collectors can make it feel unbearable. If you’re feeling overwhelmed, harassed, or even intimidated by relentless calls and threats, you’re not alone. The good news is, you have rights, and there are steps you can take to protect yourself. This guide will walk you through how to handle aggressive debt collectors, understand your legal protections, and regain your peace of mind.

What Counts As Aggressive Debt Collection?

Dealing with debt is stressful enough—aggressive debt collectors can make it feel unbearable. But what exactly counts as “aggressive”? It’s more than just persistent reminders to pay. Aggressive debt collection involves tactics that pressure, intimidate, or harass you. Here’s what to watch out for:

1. Excessive Calls

Repeated calls at all hours—early in the morning, late at night, or even during work—are a red flag. Collectors are legally required to respect your time and can’t bombard you with calls.

2. Threats And Intimidation

Threats of arrest, legal action, or losing your property are not only scary—they’re often illegal. Debt collectors can’t threaten actions they don’t intend to take or don’t have the authority to enforce.

3. Abusive Language

No one should ever yell at you, swear, or use demeaning remarks. This kind of behavior is unprofessional and violates your rights under the Fair Debt Collection Practices Act (FDCPA).

4. Deceptive Tactics

Some collectors pretend to be lawyers, government officials, or even law enforcement to scare you into paying. Others might misrepresent the amount you owe or claim you’re responsible for a debt that isn’t yours. These lies are illegal.

5. Extreme Cases (Though Rare)

In rare cases, collectors have threatened harm to pets, family members, or personal property. While these situations are uncommon, they highlight the importance of knowing your rights and taking action.

Why This Matters

Aggressive debt collection isn’t just annoying—it’s designed to make you feel powerless. But you’re not. By recognizing these behaviors, you can take steps to protect yourself. Document every call, save every message, and remember: you have the right to be treated with respect.

In the next section, we’ll walk you through your rights and the steps you can take to stop the harassment. You don’t have to face this alone.

Your Rights Under The Law: How The FDCPA Protects You

Dealing with debt collectors can feel like an uphill battle, but here’s the good news: you’re not defenseless. The Fair Debt Collection Practices Act (FDCPA) is your legal shield against abusive, deceptive, and overly aggressive collectors. It’s there to ensure you’re treated fairly and with respect—no matter your financial situation. Let’s break down exactly how it protects you:

1. No Calls At All Hours

Imagine your phone ringing at 7 a.m. or 10 p.m.—right when you’re trying to start your day or wind down for the night. The FDCPA puts a stop to that. Debt collectors can’t call you before 8 a.m. or after 9 p.m. unless you’ve given them permission. If they’re calling outside these hours, they’re breaking the law.

2. No Harassment Or Abuse

No one deserves to be yelled at, sworn at, or threatened—especially when they’re already under financial stress. The FDCPA makes it illegal for collectors to:

- Use profane or abusive language.

- Threaten violence or harm.

- Repeatedly call just to annoy or harass you.

If a collector is making you feel intimidated or unsafe, they’re crossing the line.

3. No Deception Or Misrepresentation

Some debt collectors try to scare you by pretending to be someone they’re not—like a lawyer, government official, or even law enforcement. Others might lie about how much you owe or claim you’re responsible for a debt that isn’t yours. The FDCPA requires collectors to:

- Clearly identify themselves and who they represent.

- Be honest about the debt and your rights.

- Never mislead you about the consequences of not paying.

If something feels off, trust your instincts. You have the right to ask for proof.

4. State Laws Can Offer Even More Protection

While the FDCPA sets the baseline for your rights, some states have even stricter laws to protect consumers. For example, some states limit how often collectors can contact you or require them to provide additional documentation about the debt. It’s worth checking your local regulations to see what extra protections you might have.

How To Handle Aggressive Debt Collectors: Take Control of the Situation

Now that you know your rights, let’s break down exactly how to proceed. Dealing with aggressive debt collectors can feel overwhelming, but with the right approach, you can take control of the situation and protect yourself from harassment. Here’s what you need to do:

1. Start By Documenting Everything

The first step to protecting yourself is keeping a clear record of every interaction. Write down the date, time, and details of every phone call, including the name of the collector you spoke with. Save all written communication—emails, letters, and even text messages—as these can serve as crucial evidence if you need to file a complaint or take legal action.

One of the most powerful tools at your disposal is the debt validation letter. Request this document as soon as possible. It should outline the amount owed, the name of the original creditor, and your rights under the law. If the collector can’t validate the debt, they’re legally required to stop all collection efforts.

2. Stay Calm And Keep Your Cool

It’s easy to feel emotional when faced with aggressive tactics—threats, yelling, or constant calls can rattle anyone. But staying calm is key. Remember, many threats are empty, designed to pressure you into paying quickly. Take a deep breath, focus on the facts, and don’t let them rush you into making a decision. You’re in control, not them.

3. Put A Stop To Harassment

If the calls are becoming too much, you have the right to tell the collector to stop. Sending a cease-and-desist letter is a simple yet effective way to do this. Send it via certified mail and keep a copy for your records. Once they receive it, they’re legally required to stop all communication, except to notify you of specific actions, like filing a lawsuit.

4. Explore Your Options For Resolving the Debt

If the debt is valid, and you’re able to pay, consider negotiating a payment plan or even a settlement to reduce the amount you owe. Many collectors are willing to work with you if it means they’ll recover some of the debt. Just make sure to get any agreement in writing to avoid misunderstandings later.

If negotiating feels overwhelming, or you’re unsure where to start, that’s where CuraDebt can help. We specialize in working with people just like you to navigate debt settlement and create plans that fit your unique situation. Whether it’s negotiating with collectors or exploring debt relief options, we’re here to guide you every step of the way.

When To Take Legal Action

If the harassment from debt collectors doesn’t stop, you’re not out of options. You can take action to hold them accountable. Start by filing a complaint with the Consumer Financial Protection Bureau (CFPB) or the Federal Trade Commission (FTC). These agencies investigate abusive practices and can take action against collectors who break the law.

If the collector has violated your rights under the FDCPA, you can also sue them. You may be entitled to up to $1,000 in damages, plus compensation for emotional distress and legal fees. Keep in mind, lawsuits must be filed within one year of the violation, so it’s important to act quickly if you’ve been treated unfairly.

Real Stories: How People Are Fighting Back Against Aggressive Debt Collectors

Sometimes, the best way to understand how to handle aggressive debt collectors is by hearing from others who’ve been through it. On forums like Reddit, people share their experiences, offering advice, support, and even warnings. Here are two real-life examples that highlight the importance of knowing your rights and taking action.

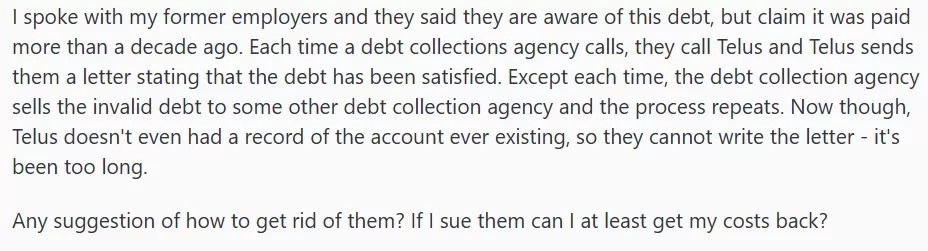

Case 1: A Decade-Old Debt That Won’t Go Away

One Reddit user shared their frustration with a debt that was satisfied over ten years ago. Despite being paid off, the debt kept getting sold to new collection agencies, each one aggressively pursuing them as if the debt were still active.

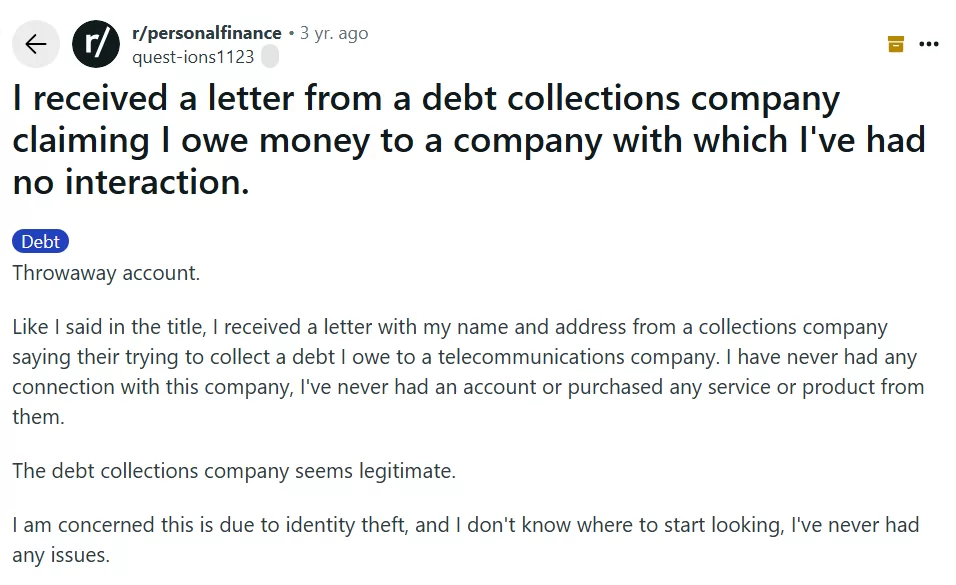

Case 2: A Debt That Was Never Theirs

Another user shared a story about being contacted for a debt they had no connection to. The collector insisted they were responsible, but the user had never heard of the creditor. Despite explaining this, the calls continued.

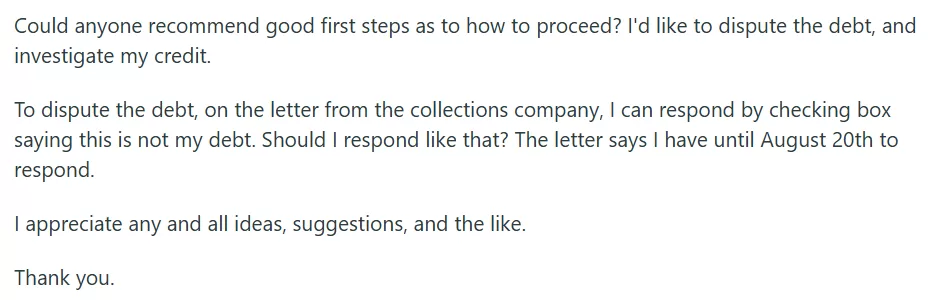

Commenters urged the user to verify the debt by requesting a validation letter.

These real-life examples show how important it is to stand up for your rights. Whether you’re dealing with an old debt that won’t go away or a debt that was never yours in the first place, the steps are the same: verify the debt, document everything, and file complaints if necessary.

Take The Next Step Toward Peace Of Mind

Dealing with aggressive debt collectors is tough—no one should face constant calls, threats, or harassment. But you’re not powerless. By knowing your rights, documenting everything, and taking action, you can protect yourself and regain control.

If the process feels overwhelming, you don’t have to do it alone. At CuraDebt, we’re here to help. Whether you need guidance on negotiating with collectors, understanding your options, or just someone to listen, we’re in your corner.

Reach out for a free consultation today. Let’s work together to create a plan that works for you and helps you move toward a brighter financial future.