The burden of debt can be a real pain, right? We totally feel you!

After all, nobody likes payments hanging on their heads like a sword, making everyday life feel like a struggle.

As you search for a way out, you might have come across two popular debt relief options: debt management and debt settlement.

They both promise to help you escape the debt trap, but their methods are worlds apart.

So what exactly is debt management vs debt settlement? And which one is better for your unique financial situation?

In today’s blog, we will answer all these questions and share insights on what people feel about both options.

Debt Management Vs Debt Settlement: A Brief Overview

While the purpose of debt management program vs debt settlement may be the same (to provide debt relief), they differ significantly in their approach.

Debt Management

Debt management is a structured program that helps individuals pay off their debt in full but with more manageable terms.

Mostly, non-profit credit counseling agencies manage debt management plans. They work directly with your creditors to negotiate lower interest rates. The goal of this program is to create a payment plan that fits your budget and doesn’t put a strain on your finances.

Under a debt management plan (DMP), you make a single monthly payment to the agency you have engaged with. The agency then distributes these funds to your creditors according to the agreed plan.

Once enrolled, you won’t be able to use your credit cards, and you won’t be allowed to open new lines of credit until the program is completed.

Debt Settlement

In debt settlement, the goal of the program is that you don’t pay the full amount of your debt to your creditors.

Instead, you take a debt settlement company on board that negotiates with your creditors to reduce the total amount of debt you owe.

The company you engage with asks you to stop paying your creditor and open a new account shared between both parties.

You make payments into this account, where they accumulate over time.

Once there are enough funds, the company negotiates with your creditors to settle your debt for less than the original amount owed.

Debt settlement allows you to potentially pay off your debts at a reduced cost. Also, you become debt-free often in a shorter timeframe than traditional repayment methods.

Eligibility Note:

You will only be eligible for either of these services if you have unsecured debt, such as credit card debt or personal loans.

So if you have secured debt, like a car loan or a mortgage, these programs are typically not applicable, as secured debt is tied to an asset that the lender can claim if payments are not made.

What Is The Difference Between Debt Management and Debt Settlement?

Now that you have a better hold on both debt relief methods, here are debt management vs debt settlement differences.

| Criteria | Debt Management Plan | Debt Settlement |

|---|---|---|

| Who Manages | Non-profit credit counseling agencies | For-profit companies |

| What Does It Offer | A structured plan to pay off debt in full over time | Negotiation to reduce the total debt owed |

| Usual Costs | An upfront cost + monthly plan fees from $25 to $75 | 15% to 25% of the owed amount |

| Risk Involved | If you open a new line of credit or miss a payment, DMP might cancel your plan. | Some creditors are not open to debt settlement deals. |

| Monthly Payments | Monthly payments are distributed to your creditors, usually lower | Payments to creditors stop. Funds are saved for settlement. |

| Best When | You want to pay off debt with lower interest rates over time. | You are in a bad financial situation and need to reduce your overall debt amount quickly. |

Debt Management Program Vs Debt Settlement: 3 Major Considerations

We’ve discussed the key differences between debt management vs debt settlement.

However, there are still three major considerations you should keep in mind if you’re planning to move forward with either of these debt relief options.

These factors can significantly influence which approach is the best fit for your situation.

1. Interest Rates and Balances

In a debt management program, interest rates play a major role. The agency you work with negotiates lower interest rates with your creditors. They often reduce them to around 6-11% on average (not everybody is lucky enough to get a low APR, though).

This reduction can make a significant difference in your monthly payments. It helps you pay off your debt in full over time (usually 3-5 years) without the burden of excessive interest.

On the other hand, Interest rates aren’t part of the equation in debt settlement. The total focus is on reducing the total balance you owe.

The company you engage with negotiates with your creditors to settle the debt for a lower amount than what you originally owed.

This means you’re not paying the full balance, and interest rates don’t play a role in the settlement process.

2. Credit Score Impact

If you enroll in a debt management program, you may or may not have an impact on your credit score. You may also have a temporary impact on your credit score, depending on the specific actions the program requires.

For instance, closing credit cards as part of the program can lower your available credit, which might reduce your score initially.

However, as you make consistent payments and reduce your overall debt, your credit score can gradually improve over time.

In comparison, in debt settlement, once your debts are fully settled, which is typically much faster than a debt management plan, you can focus on rebuilding your credit score.

Then, you can easily recover as you manage your finances responsibly going forward.

3. Timeline and Costs

Debt management programs usually take 3 to 5 years to fully resolve your debt. It’s a gradual process that requires consistency with monthly payments. You need to stay committed to the plan for it to work effectively.

As for the costs involved in debt management:

- There’s an initial setup fee paid to the agency, averaging around $40.

- A monthly fee follows, typically ranging from $25 to $30.

- Over the course of the program, you’ll pay 100% of what you owe, plus reduced interest.

On the other hand, debt settlement is relatively quicker, often taking 2 to 3 years to complete.

The plan is designed to pay less than the original amount owed to your creditors. This approach offers a faster resolution but with different financial dynamics.

Debt Management vs Debt Settlement Calculator

What Do People Think About Debt Settlement vs Debt Management?

There are many people who have benefitted from both these debt relief options.

However, your approach depends on your current financial situation and whether you have the resources to pay off your debt.

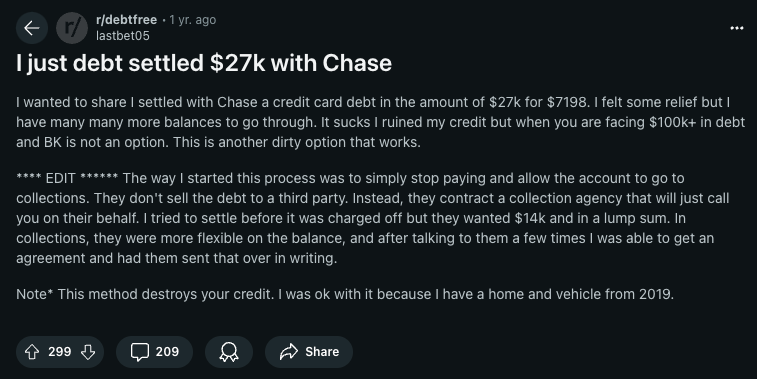

For example, one individual posted on Reddit about how he settled his debt from $27K to around $7K.

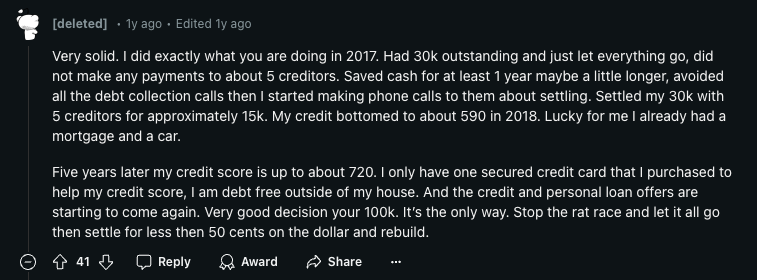

Many people resonated with his post and shared their experiences with debt settlement, like this individual:

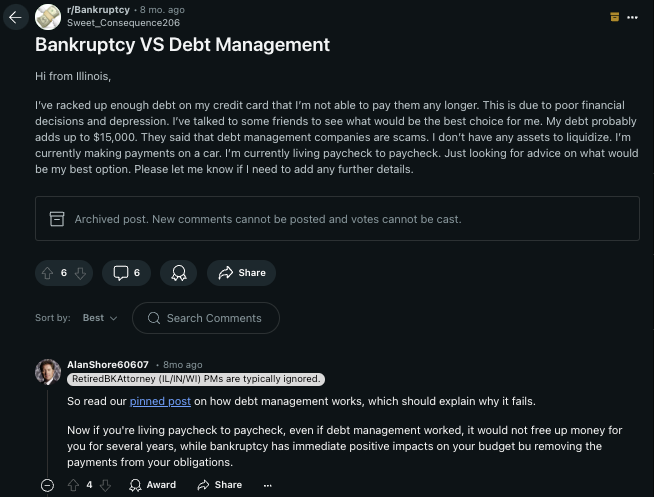

Bankruptcy vs. debt management – for instance, have a look at this Reddit thread.

The Verdict: Debt Management or Debt Settlement?

We know you’re looking for one clear-cut answer and want to know which comes out on top in the debt management vs debt settlement debate.

Well, it really comes down to your exact financial situation.

Are you in debt and feel morally obligated to pay the full amount with a monthly fee from debt management company plus interest (albeit it could be lower if your current rates are 20%+), then debt management may be something to consider.

On the other hand, are you having financial challenges and do you agree with the idea of paying back an agreed to amount (ideally as low as possible) where both you and the creditor benefit?

If your answer is yes, then debt settlement is something you should seriously consider.

With that said, if you’re leaning towards debt settlement and want to be free from debt as soon as possible, consider CuraDebt.

Over the last 24 years, CuraDebt has helped thousands of individuals regain financial stability by successfully negotiating debt settlements.

So if you’re ready to take control of your financial future, sign up for our free consultation and take the first step towards resolving your debt today.

FAQs

Is debt settlement the same as debt relief?

Yes, debt settlement is a type of debt relief where you negotiate to pay less than the full amount owed.

Is debt management the same as debt consolidation?

No, debt management involves a structured payment plan through a non-profit consumer credit counseling agency, while debt consolidation combines multiple debts into a single loan.

What is the difference between debt management and debt settlement?

In debt management, you pay the full amount to your creditor over time (usually takes 3-5 years) with interest and a monthly fee from the debt management agency. In debt settlement, CuraDebt negotiates with your creditors to pay less than the amount owed (usually takes 2-3 years depending on the amount of debt).