Personal Debt Vs. Business Debt: Which Should You Pay Off First?

Managing debt can feel overwhelming—especially when you’re facing both personal and business financial obligations. But the good news is, you have options. In this article, we’ll break down the key differences between personal and business debt, explore which one might make sense to prioritize, and help you better understand how to move forward with confidence.

Understanding Personal Debt And Its Consequences

Personal debt is any money you owe as an individual—things like credit card balances, student loans, personal loans, and mortgages. On its own, personal debt isn’t necessarily a bad thing. In fact, it can be a helpful tool when managed wisely. But when it starts to pile up or becomes hard to manage, it can take a serious toll on your finances and peace of mind.

Common Types of Personal Debt

- Credit Card Debt: With high interest rates, balances can grow fast—making it harder to catch up the longer you wait.

- Student Loans: While they often have lower interest rates, they can hang over your head for years or even decades.

- Mortgages: Generally considered a more stable form of debt, but missing payments can lead to serious consequences like foreclosure.

- Medical Bills: These often come out of nowhere and can quickly become overwhelming, especially without insurance coverage.

How Personal Debt Can Affect Your Life

- Financial Pressure: Monthly payments can stretch your budget thin, making it tough to keep up with essentials like rent, groceries, or utilities.

- Legal Trouble: If debts go unpaid, creditors may take legal action, which could lead to wage garnishment or asset seizure.

- Emotional Stress: Constant worry about money can lead to anxiety, sleepless nights, and strain on your relationships.

- Fewer Opportunities: A heavy debt load can hold you back from pursuing your goals—like buying a home, starting a business, or building savings.

The good news? You’re not alone—and there are ways to take back control. Let’s keep going and look at how business debt compares, and how to decide which to tackle first.

Understanding Business Debt and Its Impact

Business debt is a common part of running and growing a company. Whether it’s used to fund daily operations, invest in new equipment, or smooth out cash flow, taking on debt can be a strategic move. But like any financial tool, it comes with risks—especially if it becomes difficult to manage. While business debt is usually tied to the company itself, it can also affect your personal finances if you’ve signed a personal guarantee.

Common Types of Business Debt

- Term Loans: Fixed amounts borrowed and repaid over time, often used for larger investments.

- Lines of Credit: Flexible funds that you can tap into as needed for short-term expenses.

- Vendor Credit: Agreements to pay suppliers at a later date for goods or services.

- Equipment Financing: Loans or leases specifically for purchasing business tools, machinery, or tech.

How Business Debt Can Affect Your Company

- Cash Flow Struggles: Large or frequent debt payments can stretch your finances thin, leaving little room to cover day-to-day expenses.

- Growth Limitations: When too much money goes toward repaying debt, it may hold you back from hiring, expanding, or stocking inventory.

- Legal Risks: Falling behind on payments could result in creditors taking legal action or seizing business assets.

- Owner Stress: The pressure of managing debt can weigh heavily on business owners, leading to burnout and tougher decision-making.

If you’re feeling the pressure of business debt, know that you’re not alone—and there are ways to find relief. Let’s explore how to figure out which debts to tackle first.

Which Debt Should You Pay Off First?

Figuring out whether to tackle personal or business debt first isn’t always easy—it depends on your unique financial situation. The key is to take a step back, look at the bigger picture, and make a choice that supports both your current needs and long-term goals. Here are a few important things to consider:

Key Considerations

- Interest Rates

Start by identifying which debts are costing you the most. High-interest debts—like credit cards or certain business loans—can grow fast. Paying those off first can help you save a lot over time.

- Debt Size

Is there a large loan that’s close to default or creating major stress? Big debts with high stakes might need to move to the top of your priority list to avoid serious consequences like legal action or asset loss.

- Risk to Assets

If your personal or business assets (like your home, savings, or equipment) are tied to a loan, that’s something to take seriously. Focus on the debts that put what you’ve worked hard for at risk.

- Cash Flow

Your ability to cover daily expenses—whether personal or business—matters a lot. For personal finances, make sure essentials like rent, groceries, and utilities are covered. In your business, staying current on things like payroll and vendor payments is crucial for keeping operations running smoothly.

- Emotional Impact

Debt isn’t just about numbers—it can weigh heavily on your mental and emotional well-being. Some people prefer to pay off smaller debts first (the debt snowball method) to build momentum. Others aim to clear high-interest debts first (the debt avalanche method) to maximize savings. There’s no wrong choice—just what works best for you.

Other Things To Keep In Mind

- Type of Debt: Some business debts may come with tax-deductible interest or flexible repayment terms, while personal debts may carry harsher penalties or stricter deadlines.

- Future Goals: Planning to buy a home or expand your business soon? Prioritize debts that could block financing or hurt your creditworthiness.

- Creditor Willingness: Business lenders might be more open to renegotiating terms than personal creditors. Always consider what kind of flexibility is available.

Finding The Right Balance

Sometimes, the best approach isn’t choosing one or the other—it’s finding a balance. You might need to divide your resources and address both personal and business debts at the same time to maintain stability in both areas.

Whatever your situation looks like, the most important thing is to have a clear plan that works for you and your goals. Taking that first step toward clarity can make a big difference.

Smart Strategies to Manage Debt Effectively

Managing debt isn’t just about paying bills—it’s about creating a plan that fits your life and puts you back in control. Whether you’re dealing with personal or business debt, the right strategies can help you move forward with confidence.

1. Build a Repayment Plan That Works for You

A clear, consistent plan is key to getting out of debt. Here are two popular approaches you can try:

- Debt Snowball Method: Start by paying off your smallest debts first. It’s great for staying motivated because you see progress quickly.

- Debt Avalanche Method: Focus on debts with the highest interest rates first. This method saves more money in the long run, though it may take longer to feel the wins.

Pick the method that feels right for your mindset and financial goals—and stick with it.

2. Consider Debt Consolidation

If you’re juggling multiple payments, consolidating your debt might make things easier. It combines your debts into one payment, which can simplify your budget and even lower your interest rate.

Here are a few common ways to consolidate:

- Personal Loan: Use a single loan to pay off your other debts, leaving you with one monthly payment.

- Balance Transfer Credit Card: Move your credit card debt to a card with a low or 0% introductory rate, giving you time to pay it down without added interest.

While consolidation doesn’t erase your debt, it can make it more manageable.

3. Talk To Your Creditors (Or Get Support to Do It)

Reaching out to your creditors early can open the door to more manageable options. Depending on your situation, they may be willing to:

- Lower your interest rates.

- Waive late fees.

- Offer temporary relief or flexible payment terms.

That said, negotiating on your own—especially if you’re trying to reduce the total amount you owe—can feel intimidating and complex. In many cases, having a reputable debt relief company by your side can make the process smoother and more effective. These professionals understand how to communicate with creditors, negotiate on your behalf, and guide you every step of the way.

If you’re not sure where to start, remember: you don’t have to do it alone.

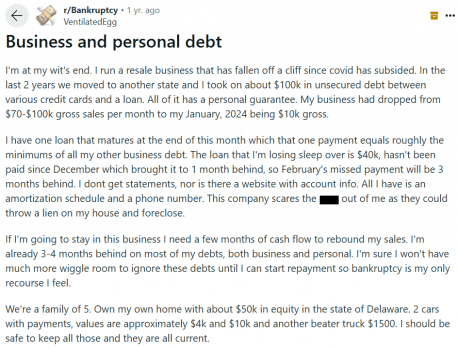

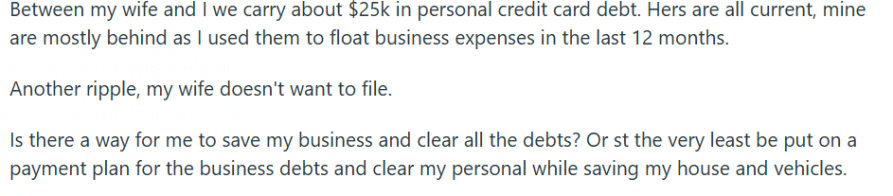

Real Experiences

Navigating debt isn’t a journey you have to face alone. Online forums like Reddit or Quora often feature stories of individuals grappling with both personal and business debt. One user shared their dilemma: facing bankruptcy due to overwhelming debt. The advice? Seek professional help before considering bankruptcy.

Bankruptcy should always be a last resort. With our help, you can explore alternatives to reduce and manage your debts effectively.

Conclusion

Deciding whether to tackle personal or business debt first isn’t always straightforward—and that’s okay. Every financial journey is different, and the “right” decision depends on your goals, your cash flow, and the risks you’re facing. What matters most is that you take steps forward with clarity and support.

At CuraDebt, we understand the stress that comes with debt—whether it’s tied to your life or your livelihood. That’s why we offer a free, no-obligation consultation designed around you. We’ll take the time to understand your situation and walk you through your options, so you can move forward with confidence.

You’re not alone in this. Let’s find the path that works best for you.