Bad debt is a common challenge for both businesses and individuals. Whether you’re running a business or managing personal finances, unpaid debts can cause serious financial strain. Luckily, there is a way to lessen the blow of unpaid debts through a tax deduction known as the bad debt deduction. This tax benefit allows businesses and certain individuals to recover some of their losses by deducting debts that have become completely worthless. Understanding how this deduction works and how to apply it can provide valuable relief, especially for businesses dealing with delinquent accounts.

In this article, we will break down the bad debt deduction, explore its types, explain how it works, and discuss how it can benefit your business. By the end, you’ll have a clear understanding of how this deduction can save you money during tax season, helping offset financial losses from unpaid debts.

Types Of Bad Debt

When considering the bad debt deduction, it’s important to distinguish between two types: business bad debt and non-business bad debt. Each type has different rules and implications for your tax filings.

Business Bad Debt

Business bad debt refers to unpaid debts that arise from operating a business. This could be loans you extended to customers or clients, sales made on credit, or other business-related transactions where the money owed was never paid. For a debt to qualify as a business bad debt, it must have been created or acquired in the course of your business.

For example, if you operate a retail business and a customer purchased goods on credit but never paid you back, this would be classified as a business bad debt. The key here is that the debt must have been related to business activities. Businesses can typically deduct bad debts in full from their taxable income, which can offer significant tax relief when properly documented.

Non-Business Bad Debt

Non-business bad debt, on the other hand, refers to debts that aren’t related to your trade or business. These are typically personal loans you may have extended to friends, family members, or other individuals, which have not been repaid.

Unlike business bad debt, non-business bad debt is treated as a short-term capital loss. This means you can only deduct the debt up to $3,000 per year, or $1,500 if married and filing separately, with the possibility of carrying over excess losses to future years. The IRS requires proof that the loan was made with repayment intent and that the debt is completely worthless to deduct non-business bad debts.

For individuals struggling with personal debts or losses, CuraDebt‘s free consultation can provide valuable assistance in navigating these complex financial situations.

How To Deduct A Bad Debt

Deducting bad debt involves key steps, and knowing the requirements helps you qualify for this tax deduction.

1. Prove The Debt Is Worthless

One of the most crucial elements of claiming a bad debt deduction is proving that the debt is worthless. For tax purposes, a debt must be completely uncollectible to qualify. This means that you’ve made reasonable efforts to collect the debt but have been unsuccessful. You must show the IRS that you’ve made efforts to recover the money, such as contacting the debtor or taking legal action.

For example, if a customer has filed for bankruptcy, this would typically render the debt worthless, making you eligible for the deduction.

2. Proper Documentation

When claiming a bad debt deduction, thorough documentation is essential. This includes keeping records of the original debt agreement, any payments that were made, communications between you and the debtor regarding the debt, and evidence of your attempts to collect the money. The IRS may request this information to verify the deduction, so maintaining organized records is important.

3. Determine The Tax Year To Deduct The Debt

For business bad debt, you can generally deduct the debt in the year it becomes worthless. It’s important to note that partial deductions are not allowed; the debt must be completely uncollectible before it can be deducted. For non-business bad debt, the debt must also be deducted in the year it becomes completely worthless.

4. Use The Correct IRS Form

For business bad debts, the deduction is typically claimed on Schedule C (for sole proprietorships) or on your business’s tax return. For non-business bad debts, the deduction is reported as a capital loss on Form 8949 and Schedule D of your personal tax return.

How Can A Bad Debt Deduction Help Your Business?

The bad debt deduction can be a valuable financial tool for businesses facing losses due to unpaid debts. When a business extends credit to customers or offers goods and services with the expectation of future payment, there’s always the risk that the debt will never be repaid. This can negatively impact cash flow, making it harder for businesses to operate smoothly. However, the bad debt deduction offers a way to mitigate these losses.

1. Reduce Your Taxable Income

One of the primary benefits of the bad debt deduction is that it reduces your taxable income. By writing off unpaid debts as a tax-deductible expense, businesses can lower their overall tax liability. This can lead to significant tax savings, which can help offset the financial impact of bad debts.

2. Improve Cash Flow Management

When businesses are dealing with unpaid debts, managing cash flow becomes more challenging. However, by taking advantage of the bad debt deduction, businesses can reclaim some of the money lost on uncollected debts, making it easier to stabilize cash flow and reinvest in growth.

3. Support Business Resilience

No business is immune to financial setbacks, and bad debts are a common occurrence for many companies. By using the bad debt deduction, businesses can soften the blow of these losses, ensuring that a single unpaid debt doesn’t derail their operations. This allows companies to stay resilient and continue to thrive despite financial challenges.

If you’re managing a business and struggling with bad debt, it’s important to explore all of your options for reducing your losses. CuraDebt offers a free consultation to help navigate debt challenges and find solutions that work best for your unique situation.

Non-Business Bad Debt And Personal Financial Health

While non-business bad debt can be frustrating, it’s important to address it both from a financial and personal perspective. These unpaid personal loans can leave you in a difficult financial position, especially if the amounts involved are significant. Deducting non-business bad debt won’t recover the full amount, but it can reduce your tax liability and offer some relief.

Real-Life Example Of Non-Business Bad Debt

For example, you loaned a family member $10,000 for a house down payment, expecting repayment over time. After a few months of payments, they lose their job and are no longer able to repay the loan. Despite your efforts to reach out and work out a payment plan, it becomes clear that you will not recover the remaining balance.

In this case, if the loan was intended to be repaid, and you can prove it’s now worthless, you may be able to deduct the unpaid portion as non-business bad debt. You can’t deduct the full $10,000 in one year, but you can deduct up to $3,000 annually until it’s fully accounted for.

To avoid non-business bad debt, treat personal loans with the same care and documentation as business loans. Ensure you have a formal agreement in place and consider the borrower’s ability to repay before extending personal loans. I

What People Are Saying On Forums

Many people turn to online communities like Reddit or Quora to share bad debt experiences, ask questions, and seek advice. We’ve gathered real-life Reddit posts about bad debts, highlighting common concerns and providing answers to frequent questions.

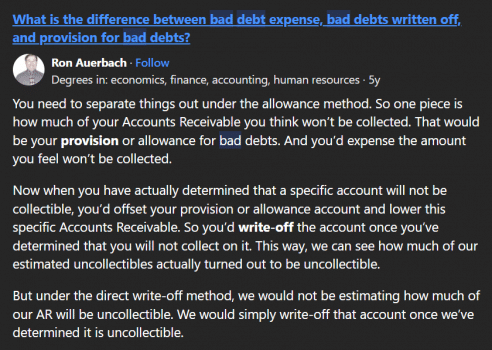

Difference Between Bad Debt Expense, Bad Debts Written Off And Provision For Bad Debts

This post explains the key differences between bad debt expense, debts written off, and provisions for bad debts. These terms are key for managing finances, as they impact how businesses handle uncollectible debts on their balance sheets.

Difference Between Good Debt And Bad Debt

This user shares valuable information about the distinction between good and bad debt. Knowing that good debt can help you grow financially, while bad debt can lead to strain, is crucial.. Understanding this difference is key to making better borrowing decisions.

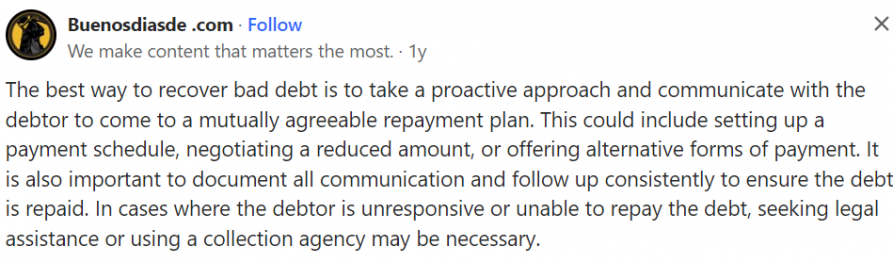

The Best Way To Recover Bad Debt

This user offers practical advice on the best methods for recovering bad debt. It’s important to be persistent and explore your options, from collection efforts to legal action, based on the debt’s size and situation.

Recovery of Bad Debts

If you want to know more about bad debts recovery, this video explains it and provides practical insights.

Conclusion

The bad debt deduction is an important tool for both businesses and individuals to help recover from the financial impact of uncollectible debts. Understanding the difference between business and non-business bad debts, properly documenting them, and using the deduction can save money and boost financial stability.

If you are dealing with debts, we can help. Take CuraDebt‘s free consultation now!